MiCA regulation has been rolled out in stages. The first stage took effect in July 2023. The requirements affecting stablecoin issuance applied from 30 June 2024, and the full MiCA framework – covering crypto-asset service providers (CASPs) – has been in force since 30 December 2024. The transitional period, during which existing providers could continue operating under national regimes while seeking MiCA authorisation, ends on 1 July 2026. After that date, any entity providing crypto-asset services to EU clients without a MiCA licence will be in breach of EU law.

EUROPEAN CRYPTO LICENSING SUPPORT. MARKETS IN CRYPTO ASSETS REGULATION – MICA.

- Crypto-asset issuance support

- Advice on crypto-asset exchange listing

- Stablecoin and e-money issuance

- Crypto Asset Service Provider CASP authorization

- Crypto exchange licensing support

- Crypto custody licensing

- Marketplaces etc.

European Markets in Crypto-Assets Regulation MiCA

The European Markets in Crypto-Assets (MiCA) Regulation has introduced a comprehensive, pan-European regulatory framework for crypto-assets. This includes an EU wide passportable Crypto-Asset Service Provider (CASP) license allowing provision of crypto related services in all EU/EEA area.

Lithuania: EU hub for crypto-asset service providers

Lithuania has emerged as a leading European jurisdiction for crypto-asset service providers, building on its established reputation in traditional finance for payment and electronic money institutions. It was one of the first EU countries to offer a transparent and cost-effective VASP (Virtual Asset Service Provider) authorization to international crypto service providers.

By the time the Markets in Crypto-Assets (MiCA) Regulation came into force, over 370 VASP companies had registered in Lithuania. ECOVIS ProventusLaw successfully guided clients through the entire licensing process, securing more than 40 VASP authorizations on an end-to-end basis.

Key Players in Lithuania’s Crypto Landscape

In 2020, Binance, the world’s largest crypto exchange, secured its Lithuanian VASP authorization. ECOVIS ProventusLaw as the main legal advisor provided comprehensive support to Binance, including Lithuanian company incorporation, VASP authorization, HR, and compliance.

In May 2025, Robinhood Europe, UAB, a subsidiary of the US-listed broker Robinhood Markets, Inc. (NASDAQ: HOOD), was granted the first Lithuanian CASP license under the new MiCA Regulation. This license is EU passportable, enabling Robinhood to offer crypto-related services across the entire European Union and European Economic Area (EU/EEA). ECOVIS ProventusLaw has played important role in legal support of Robinhood’s operations in Europe since 2023, when Robinhood Europe, UAB was initially incorporated and registered as a VASP in Lithuania. The new EU passportable CASP license replaces the previous national VASP registration, significantly extending Robinhood’s reach across the EU without requiring additional licensing in other EU jurisdictions.

Latvia: a rising star in MiCA licensing

Latvia is emerging as an attractive jurisdiction for MiCA licensing, with Latvijas Banka positioning the country as a business-friendly destination for crypto-asset service providers (CASPs). Latvia’s tax framework further supports this: under the Corporate Income Tax (CIT) regime, a 0% rate applies to undistributed or reinvested profits, with 20% applying only upon distribution.

The MiCA CASP licensing process in Latvia consists of two main stages: a pre-licensing consultation stage and a formal licensing stage. During the pre-licensing stage, Latvijas Banka provides free consultations to prospective market participants, including clarifications of regulatory requirements and advice on the application of regulation in the early stage of developing a business model. At this stage, the company does not necessarily have to be legally established and documents may be submitted in English.

During the licensing stage, Latvijas Banka conducts a 25-working-day completeness check of the application, followed by a 40-working-day substantive assessment. The review deadline may be extended if the information provided is insufficient to take a decision.

Key requirements for CASPs in Latvia include: a physical office in Latvia (virtual offices are not permitted), appointment of a dedicated AML officer with appropriate KYC/KYT systems, a board of 2–3 directors with at least one EU-resident director (a Latvian-resident director is considered advantageous), and full operational documentation including a business plan, IT security framework, business continuity plan, and internal control procedures.

The application fee for a CASP licence in Latvia is €2,500 – one of the lowest in the EU. The annual supervision fee under Article 63 of Regulation (EU) 2023/1114 is 0.6% of gross revenue, with a minimum of €3,000.

Minimum share capital requirements depend on the services provided:

- Class 1 (€50,000): crypto-asset advice, portfolio management, reception and transmission of orders, execution of orders, placing, and transfer services.

- Class 2 (€125,000): custody and administration of crypto-assets, exchange of crypto-assets for funds, and exchange of crypto-assets for other crypto-assets.

- Class 3 (€150,000): operation of a crypto-asset trading platform.

ECOVIS ProventusLaw successfully guided Backpack EU (Trek Technologies SIA) through the full end-to-end MiCA CASP licensing process at Latvijas Banka, resulting in the granting of the licence in May 2026.

MiCA Implementation Roadmap

MiCA at a glance

Objectives

- The MiCA regulation is intended to adapt the EU regulation for the digital age by enabling the use of innovative technologies in the future-ready economy

- It is set out to level out and regulate the crypto-asset industry on an EU level without curbing the development of the underlying technology

- The uniformity of EU rules will provide legal clarity in the industry in the EU and have a significant regulatory impact globally

- A harmonized EU-wide legal system will impose its requirements to all crypto-asset industry actors within its scope

- The regulation classifies market actors into crypto-asset issuers and crypto-asset service providers.

MiCA SCOPE MiCA

Crypto-assets non-stablecoin

- Utility tokens

- Crypto-assets

- Stablecoins

- NFTs, etc.

Crypto-Asset Issuers

- Crypto-assets

- Stablecoins

Crypto-Asset Service Providers

- Exchanges

- Wallet providers

- Swaps

- Payment facilitators etc.

The MiCA regulation applies to all crypto-assets and crypto market actors. Albeit, some are either completely exempted or may be exempted under certain conditions.

Exemptions and exceptions

- NFTs – Non-fungible tokens are completely exempted;

- Airdropped tokens – may be exempted under certain conditions;

- Mining / staking rewards – may be exempted under certain conditions;

- Utility tokens – may be exempted under certain conditions;

Key definitions

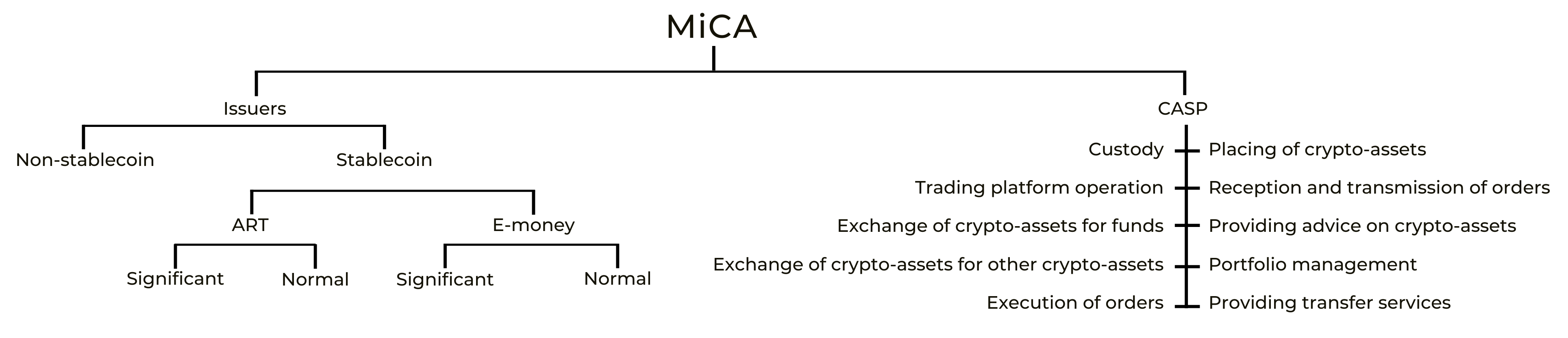

- Issuers – issuers of crypto-assets. 2 basic types: stablecoins and non-stablecoins.

- Stablecoin – a crypto-asset backed by other assets which maintain its stable value.

- Non-stablecoin – crypto-asset whose value may fluctuate depending on the market conditions.

- CASP – crypto asset service providers that provide one or multiple services prescribed by MiCA.

- E-money tokens (EMTs) – stablecoins backed by FIAT currency, equated to e-money.

- Asset Referenced Tokens (ARTs) – stablecoins backed by any assets, not equated by e-money.

- Significant stablecoin – tokens that have a significant enough market presence to influence the financial market or prevent other issuers from issuing their stablecoins.

Key takeaways

- MiCA – implemented in stages

- Possible exemptions and exceptions

- EBA urges preparation during the transitional period

- Classification of crypto-assets and market actors

- 2 types of stablecoins – EMTs and ARTs

- 10 different services for CASPs

To ensure a smooth transition, the crypto market participants should familiarize themselves with the current regulatory framework in their home member state which is still applicable during the transitional period, and use the requirements of the MiCA regulation as a blueprint for adjusting their arrangements in accordance to the upcoming regulatory regime.

Notwithstanding narrow exemptions, all crypto-asset issuers will have to prepare a white paper, including the information about:

- The issuer;

- The crypto-asset project;

- The token;

- The underlying technology including environmental effect;

- The associated risks;

Stable coin issuance

MiCA identifies two types of stablecoins – E-money tokens (EMTs) and asset-referenced tokens (ARTs). Even though they both purport to do the same thing i.e. to maintain a stable value pegged to a FIAT currency, the difference is the possible issuers and the underlying assets backing up their value.

- ARTs – can be issued by any entity, provided they are authorized to do so, and can be backed by any assets.

- EMTs – can only be issued by credit or electronic money institutions, without the need to be separately authorized, and can be backed by the FIAT currency it’s pegged to.

- Once authorized to issue stablecoins by a single EU regulator, the issuers will have the right of issuance across the EU.

- Granting interest for holding stablecoins will be prohibited.

- Both stablecoins can be considered “significant” if, among other things, their daily transaction

- volumes and market capitalization exceeds a certain threshold.

As with most crypto activities, stablecoin issuance is heavily technology-dependent that’s why it’s important to set up not only a reliable future-resistant DLT infrastructure, but also one that is compliant and has the required tracking and reporting capabilities.

CASP authorization

The provision of any of the 10 crypto-asset services is subject to an authorization by the competent authorities of the home member state. The applicant entity has to be a legal person or an undertaking with a registered office in the member state where it aims to provide at least some of its activities. The information that needs to be provided during the application process and the prudential requirements will depend on the services that the authorization is sought for.

General requirements for CASP authorization:

- Legal person, undertaking, other undertakings ensuring an equivalent level of protection as a legal person;

- Registered office in EU member state of activity;

- Effective management in the EU;

- At least one of the directors resident in the EU;

- Authorization valid across EU;

- Different rules for already licensed entities;

- Clear description of activities;

- Sound governance arrangements;

Recent MiCA licensing & authorisation cases

Trek Technologies SIA (Backpack EU)

Advised Trek Technologies SIA on its full MiCA CASP authorisation with Latvijas Banka, covering custody, exchange, order execution, and transfer services — with EU passporting across all 30 EEA states. The engagement spanned the complete application package, governance and ICT architecture, EMT regulatory boundary analysis (MiCA vs PSD2), and integration of a multinational group structure across Latvia, Lithuania, Cyprus, UAE, and BVI into a single MiCA-compliant operating model.

Trek Labs, UAB (Backpack Token)

Advised the client in connection with the preparation and notification of MiCA-compliant crypto-asset white papers in the EU for the Backpack token, filed with the Bank of Lithuania. The engagement covered the end-to-end structuring of the white paper, assessment of the token and offering model under MiCA, and regulatory engagement throughout the notification process, supporting the proposed EU-wide offering of the token.

Match Networks Ltd.

Advised the client on obtaining one of the first MiCA crypto-asset white paper approvals in the EU, filed with the Central Bank of Ireland. The engagement covered end-to-end white paper structuring, jurisdictional strategy, and full regulatory engagement through to approval — enabling a regulated EU-wide token offering.

Proof Space Pte. Ltd.

Advised the client on one of the first MiCA crypto-asset white paper notifications filed with the Bank of Lithuania, enabling EU-wide token offering and admission to trading. The engagement covered end-to-end white paper structuring and submission, regulatory communications, and iterative supervisory feedback.

Aethir Network Foundation Company

Advised the client on obtaining MiCA white paper approval from the Central Bank of Ireland, enabling EU-wide token offering and distribution. The engagement covered full white paper preparation and submission for a technically complex token structure — notably, the Central Bank requested no amendments, reflecting the quality of the submission.

MiCA restructuring of a Lithuania-based crypto-asset business (confidential client)

Advising a Lithuania-based crypto-asset business on restructuring its operating model from a legacy VASP intermediary framework to full MiCA CASP compliance. Fundamental redesign of governance, outsourcing structures, operational substance, and regulatory accountability to support CASP authorisation with the Bank of Lithuania.

MiCA CASP remediation and resubmission for a Lithuania-based crypto-asset business (confidential client)

Advising a legacy VASP on restructuring its regulatory framework following a Bank of Lithuania request to withdraw its initial CASP application due to governance and substance deficiencies. The engagement covers full gap analysis, redesign of custody infrastructure, outsourcing and ICT governance, and organisational substance — with the objective of preparing a materially strengthened resubmission under MiCA.

Practice Areas

Crypto currency exchange license

Contact person

Newsletter Subscription

Newsletter Subscription